Want to crush your debt faster, automate personal finances, save hundreds or even thousands per month (and still buy what you love), and understand why buying a house might not be the wisest move? Follow along as we explore the wisdom of Ramit Sethi‘s “I Will Teach You to Be Rich,” presenting a contemporary, straightforward guide to taking control of your money matters. Let’s uncover some of the essential concepts highlighted within the book:

Key idea No. 1: Stop Making Excuses

Saving money is something many people struggle with, but it’s also something that’s crucial for managing your personal finances and peace of mind. If you find yourself making excuses for not saving, it’s time to take action and overcome those obstacles.

First things first, it’s time to take responsibility for your financial education. Instead of blaming external factors like the media or the education system, recognize that learning about finances is ultimately up to you. Take the initiative to educate yourself by reading books, listening to podcasts, or attending workshops on personal finance. The more you know, the better equipped you’ll be to make smart financial decisions.

Another excuse is the fear of losing money. It’s natural to be cautious about investing or saving, but it’s important to remember that every mistake is a learning opportunity. Starting small and gradually increasing your savings can help ease this fear and build confidence over time.

Decision paralysis is also a common issue in money management, where individuals feel overwhelmed by all the choices they have to make, which can lead to procrastination or avoiding decisions altogether. To beat this, it’s important to simplify things. Focus on your main financial goals and break big decisions into smaller, easier steps. This way, you can take control and move forward with confidence.

Finally, it’s crucial to avoid falling into the trap of victim mentality. Instead of making excuses for why you can’t save money, take ownership of your financial situation and empower yourself to make positive changes. Remember that it’s never too late to start saving, and every small step you take towards financial stability is a step in the right direction.

Key idea No. 2: Master Credit Card Usage

Credit cards can be a great first step towards manage your personal finances. Credit cards allow you to make big purchases even if you don’t have the money upfront, but it’s important to keep in mind two crucial factors: your credit report and credit score.

Your credit report tracks your credit activity and provides information to potential lenders, while your credit score is a number between 300 and 850 that reflects your creditworthiness. A good credit score can make you more attractive to lenders, resulting in better loan interest rates. In fact, having a good credit score can save you thousands of dollars in interest over the years.

Let’s look at an example. With a good credit score of 750-850, you would pay $359,867 in interest on a $200,000 mortgage over 30 years. However, if you have a bad credit score of 620-639, you would have to pay $430,427 to pay it off, that’s an extra $70,000!

Here are six commandments to help you optimize your credit card usage, improve your credit score, and earn rewards.

Firstly, pay your credit card bills regularly. Your payment history accounts for 35% of your credit score, so it’s important to pay on time. You can set up automatic payments to avoid missing any bills, which can cause a drop in your credit score.

Secondly, try to get any fees waived. Call your credit card company and ask if you’re paying any fees, including annual fees or service charges. If they can’t waive the fees, consider switching to a no-fee card.

Thirdly, negotiate a lower annual percentage rate (APR). Your APR is the interest rate your credit card company charges you. Call and negotiate for a lower APR to avoid high-interest payments and save money.

Fourthly, know your credit score. Your credit score can impact various aspects of your life, so it’s important to monitor and improve it.

Fifthly, keep your credit utilization low. It’s a good idea to keep your credit utilization below 30% to show lenders that you’re responsible with credit.

Lastly, only apply for credit when you need it. Applying for credit too often can negatively impact your credit score, so it’s best to apply only when you need it and avoid opening too many accounts at once.

By following these commandments, you can optimize your credit usage and enjoy the benefits of credit cards while avoiding any negative consequences. Remember, paying your bills on time and keeping your credit score high can save you thousands of dollars in the long run.

Key idea No. 3: Start Investing Today

Saving money is great, but investing can help you take it even further. And a 401K retirement fund is an excellent place to start! It’s simple to set up, and you can authorize a portion of your paycheck to be automatically sent from your employer to your 401K. The benefits of having a 401K include tax advantages, employer matching contributions, and low maintenance.

But don’t stop there! You should also consider opening a Roth IRA, which allows you to invest in whatever you want, like individual stocks and index funds. Unlike a 401K, a Roth IRA uses after-tax dollars, so you won’t be taxed on your interest earned or withdrawals during retirement.

Investing your money wisely can help you achieve your financial goals and provide a comfortable retirement. So, start investing today and watch your money grow!

Key Idea No. 4: Budget Strategically to Manage Personal Finances

Are you tired of feeling guilty every time you swipe your card? Do you struggle to find a balance between treating yourself and being financially responsible? If so, you’re not alone. Many people face this dilemma on a daily basis, but there is a solution: the Conscious Spending Plan.

A Conscious Spending Plan is a strategy for managing your money that allows you to spend guilt-free on the things that matter most to you. It splits your spending into chunks. 60% for stuff like rent and bills, 10% for smart investments, another 10% for unexpected stuff or trips, and the sweet 20%? That’s for splurging without the guilt.

The beauty of a Conscious Spending Plan is that it’s tailored to your personal priorities. If travel is your passion, you can allocate more money to your vacation fund. If you’re a foodie, you might want to budget more for dining out. It’s important to remember that conscious spending isn’t about being cheap. It’s about making your own decisions about what’s worth spending on and what’s not.

Key idea No. 5: Rethink Big Purchases

Big purchases like a new car or your first home can feel overwhelming, but with the right approach, you can make smart decisions and save money.

Let’s talk cars first. When thinking about buying a car, don’t just focus on the brand or mileage. Think about how long you plan to keep it. Choosing a reliable car, taking good care of it, and driving it for a long time can save you a lot of money.

Now, onto houses. Buying one is a big deal and needs some serious thought. Do your homework on the market, understand how buying works, and learn a bit of real estate talk. But hold up, who should even buy a house?

First and foremost, you should buy a house only if it makes financial sense. In the old days, this meant that your house would cost no more than 2.5 times your annual income. However, things are different now. You can stretch these traditional guidelines a little, but you shouldn’t buy something you can’t afford.

Buying a house is a complex process, and it’s essential to know what you’re getting into. Take the time to do your research and educate yourself on the process. Ensure that you can afford at least a 20 percent down payment and that your monthly payments don’t exceed your budget. Don’t set unrealistic expectations; start with a starter house, and work your way up from there. By doing so, you’ll avoid financial pitfalls and enjoy the dream of home ownership.

Key idea No. 6: Simply Invest & Ignore Experts

Investing can be pretty overwhelming, especially when you’re bombarded with tons of financial advice and predictions from experts. It can make you feel like you need a degree in finance just to understand it all. Plus, the market is unpredictable, which can add to the confusion of investors.

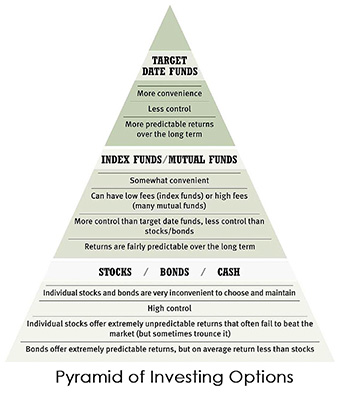

But here’s the good news, there’s a simple and effective approach to investing that anyone can use, regardless of their financial knowledge. It’s called the Pyramid of Investing Options. Imagine a pyramid with different investment categories, and at the base are basic investments like stocks, bonds, and cash. In the middle are index and mutual funds, and at the top are lifecycle funds. As you move down the pyramid, the investments become more complex.

The easiest way to invest is through automatic lifecycle funds, which adjust their allocation of stocks, bonds, and cash based on your age. This simple approach can help you feel confident in your investment decisions without being overwhelmed by all the noise from the experts.

Now, the myth of financial expertise is that even experts cannot predict the future of the market. It’s a game of chance, even for the most seasoned fund managers. So, paying high fees for unreliable expertise is not worth it when you can take control of your own financial future. It’s time to simplify our approach to investing and stop relying on experts who cherry-pick their successes.

The good news is that investing is for everyone, and you don’t need a lot of money to get started. Automatic investing is a simple and effective way to invest in low-cost funds. By automating your investments, you can sit back and relax while your money grows. Plus, automatic investing lowers expenses, which is essential for investment performance. You can focus on living your life instead of worrying about your money.

At the base of the Pyramid of Investing Options are basic investments such as stocks, bonds, and cash. Stocks can provide excellent returns averaging about 8 percent per year, but it’s best to choose funds instead of investing all your money in one stock. Bonds offer a guaranteed rate of return and provide a reliable income stream, and they let you decrease the risk in your portfolio. However, the return on bonds is generally lower than it would be on stocks.

So, in conclusion, automatic investing is a simple and effective way to grow your wealth without requiring too much time and attention. It’s important to stick to your investment plan and resist the urge to make changes during turbulent times. By choosing the right investments and using automatic investing, you can get rich. And remember, investing doesn’t have to be complicated, it’s for everyone!

Key Idea No. 7: Master Love and Money

Managing personal finances is important, but it’s even more critical to know how to handle money with the people around you. Whether it’s dealing with friends who never tip or discovering your parents’ debts, love and money play out in all sorts of situations.

One crucial aspect to consider is the intersection of love and money. In any relationship, whether romantic or friendly, finances are bound to play a role. From deciding who pays for dinner to sharing household expenses, money can often be a source of tension or misunderstanding. Recognizing this intersection and finding ways to navigate it with grace and understanding is essential for maintaining healthy relationships.

Another challenge in managing personal finances is dealing with the overwhelming amount of advice and opinions that bombard us daily. From well-meaning family members to financial gurus on social media, everyone seems to have an opinion on how we should handle our money. While some advice may be helpful, it’s crucial to filter out the noise and focus on what aligns with our own values and goals.

In conclusion, mastering personal finance is essential for taking control of your financial well-being. By embracing responsibility, avoiding victim culture, and adopting smart strategies like conscious spending and wise investing, you can pave the way towards achieving your financial goals and securing a comfortable retirement.

If you’re eager to delve deeper into these key concepts and embark on a journey to financial empowerment, don’t hesitate to explore “I Will Teach You to Be Rich” by clicking here.

Leave a Reply