Ever find yourself lost in the maze of investing, wondering where to put your hard-earned cash, and if saving alone is cutting it? Well, buckle up for a financial odyssey as we dive into a fresh perspective on building wealth. Nick Maggiulli’s “Just Keep Buying” takes center stage, unveiling a no-nonsense strategy that’s all about steadily stacking up income-producing assets. Forget the market timing anxiety – this book’s mantra is to embrace dollar-cost averaging like a boss. Get ready to ride the waves of financial wisdom as we explore a path to prosperity that’s as simple as it is effective:

Key Idea No 1: Poor Save, Rich Invest

Navigating the financial landscape can be tricky, especially when it comes to finding the right balance between saving and investing. Many people tend to get caught up in the intricacies of investment analysis, overlooking the fundamental aspects of income and spending.

The crucial point is to understand that your financial priorities should align with your current circumstances. Whether you have a small or substantial portfolio, your focus needs to adapt accordingly. Your focus depends on your financial situation. If you’re starting small, focus on saving and investing. If you’re wealthier, fine-tune your investment strategy. In other words, saving is for the poor, investing is for the rich.

Now, let’s figure out where you stand. Try this simple calculation: compare your expected savings to expected investment growth. If savings are higher, focus on saving and investing; if investment growth wins, refine your investment strategy.

As you age, shift your focus from savings to investments. Consider a 40-year journey, saving $10,000 a year with a 5% return. Initially, savings dominate, but in later years, investments contribute significantly more to growth. The Save-Invest continuum is crucial. If you’re asset-less, focus on saving. If retired, dive into investments. For everyone else, it’s a balance.

In conclusion, finding the right balance between saving and investing is a dynamic process. By understanding the Save-Invest continuum and tailoring your focus to your current financial situation, you can make informed decisions that align with your long-term goals. Remember, it’s not about one-size-fits-all solutions; it’s about adapting your strategy to your unique financial journey.

Key Idea No. 2: How Much Should You Save

In the world of saving money, the old rule of putting away 20% might not cut it anymore. Life is full of twists and turns, and everyone’s financial situation is different. Let’s talk about a more personalized approach to savings without all the confusing jargon.

You see, the idea of saving a fixed percentage doesn’t always fit with the real world. Studies tell us that not everyone can sock away the same amount. The lower earners manage about 1%, while the top 20% save 24%, and the top 1% save 51% annually. That’s a huge gap! The usual saving advice tends to overlook these differences.

Think about it – life happens. Changing jobs or careers can turn your 40% savings rate into a measly 4%. It’s a reminder that life doesn’t follow strict rules. The key is to be flexible and save what you realistically can, considering your unique circumstances. No need to stress over a one-size-fits-all approach.

Money stress is a big deal for most folks. Surveys show that Americans worry a lot about their finances, and saving is a major part of that stress. But here’s the deal – worrying about not saving enough can be worse than the actual saving. So, let’s keep it chill and focus on what you can save without losing sleep.

Now, here’s a simple way to figure out how much to save: Savings equals Income minus Spending. Break down your monthly income and fixed expenses, and you’ve got a solid estimate of what you can save. Sure, tracking every dollar is great, but just knowing your fixed costs and making educated guesses for the rest will do the trick.

And guess what? Contrary to common beliefs, retirees often worry about running out of money rather than overspending. Studies show that retirees tend to maintain or increase their financial assets over time, leaving substantial wealth for heirs. This challenges the notion that people need to save more than they think.

Key Idea No. 3: How to Save More

In the world of personal finance, there’s an ongoing debate: Should you focus on cutting expenses or boosting your income? One camp advocate meticulous spending control, arguing that small savings, like making coffee at home, can accumulate to substantial wealth. On the flip side, the opposing faction champions growing income through side hustles, asserting it’s easier than scrutinizing every expense.

Both arguments have their merits because, at the end of the day, your savings boil down to your income minus your spending. But here’s the catch: cutting spending might not be as effective as it seems. If we look at the Consumer Expenditure Survey for U.S. households, it’s clear that for many, especially those in lower income brackets, trimming expenses on essential items is just not doable.

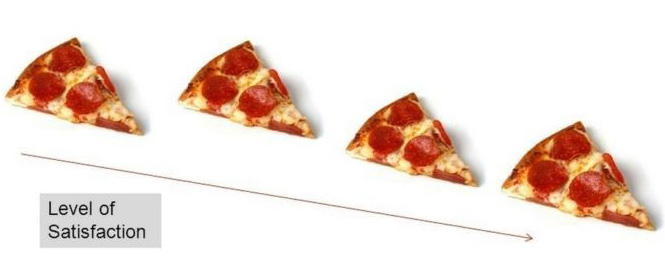

Take the bottom 20% of earners, for example. They consistently spend more than what they bring in after taxes on basics like food, housing, healthcare, and transportation. So, why doesn’t spending increase proportionally with income? Well, it’s all about something called diminishing marginal utility – kind of like how each additional slice of pizza brings less joy. Higher-income households spend a smaller percentage on necessities relative to their income.

Despite this, mainstream financial media keeps pushing the idea that cutting spending is the magic solution to getting rich. The problem is, these stories conveniently overlook the need for extraordinary investment returns and a rock-solid investment strategy, which are often out of reach for many.

So, let’s unveil the biggest lie in personal finance – getting rich isn’t mainly about cutting spending. Research shows that initial wealth, not motivation or talent, is what keeps people out of poverty. Studies from different countries back this up, highlighting the difficulty of breaking free from a poverty trap due to limited resources.

Alright, so how do you truly build wealth? The key is to boost your income and invest in things that generate more income. Sure, reviewing your spending habits is important, but the focus should be on tightening where you can and, more importantly, increasing your income.

To bump up your income, think about selling your time or skills, marketing a service, teaching online, creating a product, or moving up the corporate ladder. Yes, increasing your income might be tougher initially than cutting spending, but it sets the stage for long-term wealth.

But here’s the thing – these strategies are just stepping stones. The real goal is to use that extra income to get income-producing assets. Ownership is the path to serious wealth, going beyond just earning a paycheck.

In a nutshell, building wealth is more than just trading your time or skills for money. It’s about ownership – turning what you have into financial capital by acquiring assets that bring in income. So, if you want to start this journey, start thinking like an owner.

Key Idea No. 4: Why Should You Invest?

Investing isn’t just about numbers; it’s about building a secure future for yourself. Let’s break down three reasons why diving into the world of investments is a game-changer:

- Reason 1: Saving for your future-self: Imagine investing as the blueprint for your future self – the one you dream of. It’s like creating a financial safety net for the time when your working days are behind you. Studies even show that picturing this future-self boosts your commitment to long-term investing.

- Reason 2: Preserving Wealth Against Inflation: Inflation is like a sneaky villain silently stealing the value of your money. But guess what? Investing is your superhero cape against this financial nemesis. When your assets grow faster than inflation, they become your shield. History is full of examples proving that investing is a champ at preserving and growing wealth.

- Reason 3: Replacing Your Human Capital with Financial Capital: You know all those skills, knowledge, and time you have? That’s your human capital. But here’s the thing – time is limited. Investing is like a magical time-bending trick, turning your diminishing human capital into long-lasting financial capital. Think of it as a reservoir of income waiting for you when the 9-to-5 grind is a thing of the past.

So, investing isn’t just about numbers and graphs; it’s about securing the life you’ve always envisioned. It’s like building a bridge to your future self, protecting your wealth from invisible threats, and turning your skills into a financial powerhouse.

Key Idea No. 5: Just Keep Buying

Embarking on the stock market journey is like a thrilling ride through time, where your strategies act as the compass guiding your financial adventure. Forget about trying to time the market perfectly – the golden rule is to just keep buying, no matter where the market stands.

The tempting idea of catching stocks at their absolute lowest might seem exciting, but historical evidence suggests that DCA outshines the “Buy the Dip” approach in over 70% of 40-year stretches. Don’t get caught up in the wild goose chase of finding the perfect dip. The real power lies in consistently and wisely investing over time.

Similarly, Market volatility might sound like a scary beast, but avoiding it completely means missing out on opportunities. Striking the right balance – facing some ups and downs while steering clear of major plunges – is the entry fee for stock investors. Think of diversification as your superhero cape, combating volatility while understanding that market rollercoasters are part and parcel of the investment game.

In a world where financial strategies are as diverse as the people using them, this journey is all about disciplined investing. From the reliable track record of DCA to the influence of luck and the necessity of embracing market twists, the bottom line is crystal clear: Just Keep Buying. With a steady, informed, and disciplined approach, investors can conquer market challenges and build enduring wealth over time.

Key Idea No. 6: When Should You Sell?

Investing can sometimes feel like navigating a maze, especially when it comes to the tricky decision of when to sell. It’s not as easy as it sounds because you’re dealing with the fear of missing out on gains and the fear of losing money. To keep your emotions in check, it’s wise to establish some selling rules beforehand. Let’s dive into three situations where selling might be the way to go:

First up, we’ve got “Rebalancing.” Imagine your investment portfolio as a seesaw, perfectly balanced. Over time, without adjustments, it can lean heavily on one side due to changing market values. Rebalancing helps you bring things back to your original plan, reducing risks and keeping your investments in check.

Next, picture this: you find yourself in a situation where a large chunk of your wealth is tied to one stock. It’s like having all your eggs in one basket. While it’s great to celebrate those gains, it’s also smart to diversify. Selling a bit over time can be a savvy move, reducing risk without putting all your potential gains on the line.

Now, let’s talk about “Meeting Financial Needs.” The whole point of investing is to create the life you want. Whether you’re eyeing that dream retirement or saving up for a big purchase, selling assets can be the golden ticket to achieving your goals. After all, what’s the point of investing if you can’t enjoy the results?

There’s a saying in the investment world, “Buy quickly, sell slowly.” While jumping into investments might be the go-to move, selling gradually is often the smarter choice. It may not be flawless, but it can help you make the most of your returns.

Remember, in the game of investing, it’s not just about making money; it’s about making the money work for you. Set your rules, stick to them, and make sure you have enough money to cover your essential living expenses before taking risks to achieve your desired lifestyle. Because, at the end of the day, isn’t that what investing is all about?

In summary, Nick Maggiulli’s “Just Keep Buying” advocates a straightforward approach – consistently acquiring income-generating assets through dollar-cost averaging. It challenges conventional wisdom, highlighting the importance of personalized savings, income growth, and the crucial role of investing.

Explore the insights of “Just Keep Buying” by clicking here. Amidst various financial strategies, this book stands out as a guide for disciplined investors, emphasizing that continuous buying is the key to success.

Leave a Reply